The process of converting from VAS to IFRS in financial statements is an important step to help businesses improve transparency, accuracy and compliance with international practices. This process not only requires a deep understanding of accounting standards but also requires careful preparation and implementation in specific stages. Here are four stages of the conversion process from VAS to IFRS that businesses need to pay attention to.

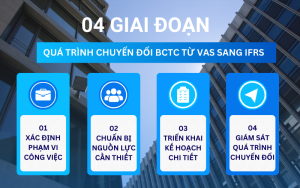

Determine the scope of work

Assess the current situation and differences

The first step in this stage is to conduct a detailed assessment of the current status of the business’s financial statements according to VAS. This process includes comparing the current accounting standards under VAS with the requirements of IFRS. The differences need to be clearly identified, as they will directly affect decisions during the conversion process. For example, IFRS often requires the recognition of assets and liabilities at fair value, while VAS may allow the use of historical values. Failure to recognize this difference can lead to errors in the conversion process.

Planning the conversion

After assessing the current situation, the enterprise needs to develop a detailed plan that includes the steps needed to convert. This plan should clearly identify the stages, the resources required, and the expected time for each step. A study by PwC shows that thorough conversion planning can reduce the time and cost associated with IFRS conversion by 20-30%. This is especially important for large enterprises with complex financial structures, where small mistakes can lead to large consequences in terms of cost and time.

Identifying the financial statements that need to be converted

Not all financial statements need to be converted immediately. Enterprises need to identify which reports need to be converted first, and which reports can be converted later. Consolidated financial statements may be the first priority due to their importance in providing an overview of the financial position of the entire group. Other reports such as the cash flow statement or the income statement may be considered for conversion at later stages, depending on the complexity and requirements of the business.

Read more: Vietnamese enterprises prepare for IFRS financial statement conversion: Time is running out?

Prepare necessary resources

Recruit and train staff

The transition from VAS to IFRS requires in-depth knowledge of international accounting standards, because the difference between the two systems lies not only in the way of recording and reporting financial statements but also in the way businesses assess and manage financial risks. Therefore, recruiting and training staff is a prerequisite. This not only helps businesses ensure the accuracy of financial statements but also helps employees improve their professional capacity, contributing to the sustainable development of the company.

Prepare support tools

The difference between VAS and IFRS not only requires a change in knowledge but also requires support tools to be upgraded or replaced to meet new requirements. Accounting software, financial analysis tools and data management systems need to be updated to comply with IFRS standards. Although the initial cost is quite high, this helps businesses avoid legal risks and increase transparency in business operations.

Updating information technology systems

To ensure that new processes are integrated smoothly and data is continuously managed, IT systems need to be adjusted or upgraded. This includes improving IT infrastructure, upgrading management software and integrating IFRS support tools into the current system. Upgrading the IT system not only meets the requirements of IFRS but also improves data management efficiency and minimizes risks in financial operations.

Implementing the plan

Establishing new processes and systems

Businesses need to establish new accounting processes in accordance with IFRS. These processes not only ensure compliance with new regulations but also integrate smoothly with the current financial management and reporting systems. This requires not only a large financial investment but also time, especially for businesses with complex and diverse systems.

Adjusting accounting policies

When converting to IFRS, businesses need to review and adjust all current accounting policies. These changes may include the way revenue, expenses, assets and liabilities are recognized. This can make a big difference in financial reporting compared to traditional methods under VAS. Businesses will have to change the way they account for and make provisions, directly affecting reported profits

Preparing financial statements according to the new standard

This is an important testing step to ensure that all the requirements and principles of IFRS are fully complied with. Businesses need to prepare comparative reports between VAS and IFRS to assess the differences and make appropriate adjustments. Businesses often have difficulty converting their initial financial statements, especially at the stage of preparing the opening balance sheet according to IFRS.

Read more: Solution for businesses converting from VAS to IFRS

Monitoring the transition process

Monitoring and evaluating effectiveness

Monitoring the transition process plays a key role in ensuring that businesses can detect and promptly resolve issues that arise during the implementation process. To effectively monitor, businesses need to build a strict monitoring system, including performance measurement indicators such as: time to complete reports, error rates in financial statements, and compliance with new standards.

Ensuring full compliance

Ensuring that all financial processes and reports comply with IFRS regulations is an indispensable factor in the transition process. This requires businesses to organize internal audits or hire independent auditors to check and evaluate compliance. Organizing periodic audits helps increase transparency and ensure that businesses are on the right track in applying IFRS.

Improvement and refinement

After completing the initial conversion process, businesses need to continue to improve and refine related processes to ensure long-term sustainability and effectiveness. The application of IFRS is not just a one-time task but a long-term commitment, requiring continuous updating and adjustment to respond to changes in the business environment and international regulations. This includes regular reassessment of accounting processes, updating software and support tools, and improving staff expertise.

This conversion not only helps businesses comply with international regulations but also facilitates investment attraction, improves management efficiency and optimizes costs. Statistics from the World Bank show that businesses applying IFRS are often 30% more likely to attract foreign investment than businesses that only comply with domestic accounting standards. This is especially important in the context of international economic integration.

Read more: Giải pháp báo cáo tài chính hợp nhất tự động 99% quy trình